Since the global financial crisis of 2008, emerging market economies have experienced a surge in capital flows in response to significant monetary easing by major central banks. Gross capital inflows to the Middle East and North Africa (MENA) have remained high compared to other emerging markets, but their composition has changed significantly, with a surge in portfolio flows (equity and bond instruments) and a decline in foreign direct investment.

Capital flows are a boon to the region in a variety of ways. They can serve as a source of financing for countries and contribute to job creation for a fast-growing population.

With global economic risks now on the rise, MENA countries would be particularly vulnerable if global risk sentiment shifts.

But the region’s economies must do more work to ensure the benefits of portfolio inflows while securing more stable and growth-friendly foreign direct investment, our research shows.

Sharp rise in flows

With the increased integration of MENA countries into global capital markets, portfolio and bank inflows to the region surged to more than $155 billion over 2016–2018. That accounted for nearly 20 percent of total portfolio flows to emerging economies during those two years and was about three times the volume of flows to MENA countries over the previous eight years.

Why have portfolio flows to the region increased so sharply? We find that about two-thirds of the increase can be attributed to a more favorable global risk sentiment that is notably below its historical average as measured by the VIX, a widely watched measure of US equity market volatility. Portfolio inflows are mostly driven by global “push” factors, such as financial market risk sentiment.

But other factors have also been at play. Large fiscal and external deficits resulting from increased spending in such countries as Egypt, Jordan, Lebanon, and Tunisia have contributed to this trend, as has lower revenue in oil exporters such as Bahrain and Oman after the 2014 oil price shock. Capital inflows have helped governments finance these deficits. The recent inclusion of Gulf Cooperation Council countries—Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates—in global bond and equity indices has also been a factor contributing to the rise in portfolio flows to the region.

Heightened vulnerability

Overall, the region has benefitted from a generally favorable environment for such inflows. However, with global economic risks now on the rise, MENA countries would be particularly vulnerable if global risk sentiment shifts—especially those with large fiscal deficits, high debt burdens, and limited buffers.

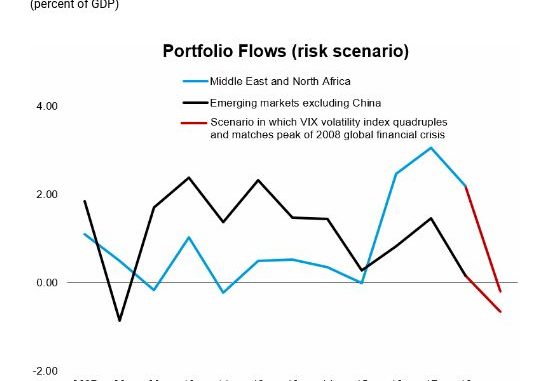

Our research finds that portfolio inflows to the region are nearly twice as sensitive to changes in global risk sentiment as compared with other emerging economies, which could lead to capital flight during high-risk periods. This sensitivity most likely stems from the higher perceived overall risk of the region, reflecting geopolitical uncertainties, reliance on volatile oil prices, and exposure to global trade tensions.

To put this in perspective, we calculate that if the VIX doubled from its 2018 level, portfolio inflows to the MENA region would be halved. If the volatility measure quadrupled from 2018 to its peak during the global financial crisis, portfolio flows could come to a complete halt.

Building resilience

In light of this heightened risk, what should MENA countries do to strengthen their resilience to volatile flows?

One important lesson from emerging market economies is that improved policy frameworks are crucial not only in attracting but also in preserving capital flows, while helping mitigate the risk of outflows. Several countries in the region are making progress on reducing economic vulnerabilities, which strengthens their resilience to adverse economic shocks and helps lessen their need to borrow. Egypt has taken important steps in establishing inflation targeting, for instance, while Morocco and Pakistan have made progress in allowing more flexible exchange rates. Ensuring stable macroeconomic conditions by reducing fiscal deficits will be critical to insulating the region’s countries from capital flow volatility.

Countries will also need to undertake certain key structural reforms, including measures to strengthen financial supervision and regulation as well as enhance or develop sound macroprudential toolkits to improve the capacity of the financial system to safely intermediate cross-border flows. Such toolkits should include policies to ensure adequate capital and liquidity buffers in banks as well as contain their exposure to particular sectors or assets, such as real estate or foreign exchange. In countries where large capital inflows lead to a consumption boom and thus put pressure on exchange rates and other asset prices, greater exchange-rate flexibility supported by sound macroeconomic policies could act as a shock absorber.

Nonetheless, recent experience from emerging markets also shows that push factors from advanced economies have intensified to the point that they are now complicating the ability of domestic policy frameworks to cope with large capital flows. And while the surge in portfolio flows to the MENA region is still nascent, countries could start building resilience to the prospect of large stocks of foreign equity and bonds relative to the size of their economies. By further developing domestic capital markets—including through the establishment of a well-functioning government bond market—governments would encourage a more stable domestic investor base, improve competition, and foster corporate debt markets.

Of course, these reforms will take time. But demonstrating a strong commitment to such policies would send a clear signal to investors, which could lead to immediate positive effects. By deepening their understanding of the composition of capital flows, countries throughout the region can ensure that their economies benefit from inflows rather than face added risk..

[“source=blogs.imf.org”]