Many millennials ask if they will ever be rich with those small shots of investment every month. Be it a recurring deposit or a systematic investment plan in an equity mutual fund, most financial planners advise investments in a disciplined manner to achieve seemingly unachievable goals depending on the time on hand and the risk profile of the investor. While individuals look for investments offering the highest possible rate of return, the tenets of personal finance however, ask investors to invest as much as possible for as long as possible.

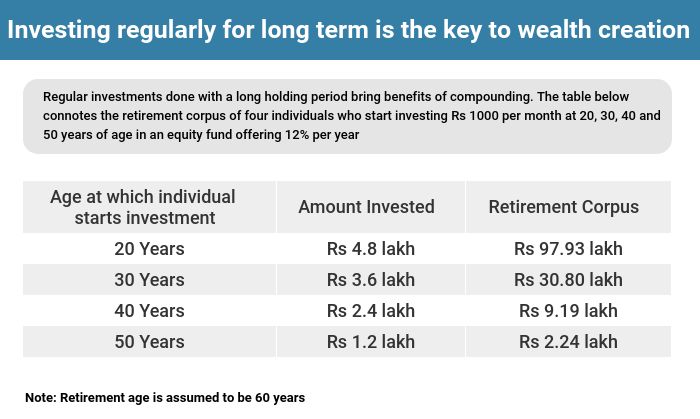

This very basic input may not attract many followers. But in the reality this simple action of being regular with your investments can help you build large corpus. Let’s try to understand this with an example. There are four individuals who decide to invest each month till they retire at the age of 60 years. Their current age is 20, 30, 40 and 50 years. Each one of them decide to invest Rs 1,000 per month, a modest sum till the age of their retirement, in an equity mutual fund offering 12 percent rate of return per year. Here is how their corpus would look like when they retire.

If one starts investing Rs 1,000 per month at the age of 20 years and keep investing till he turns 60, he will accumulate a corpus of Rs 97.93 lakh. If one starts at the age of 30 years, then he will build a corpus of Rs 30.8 lakh. Everyone would like to retire like the 20 year old in the above example does. A point to note here is that all four of them have enjoyed the same rate of return – 12 percent per year. The exponential growth the 20 years old enjoyed is an outcome of the compounding the money sees over a long period of time of 40 years. The longer you let your money work hard, the more money you take home. If you keep investing your monthly commitment, you will walk away with a large sum.

Let’s make a small change to this calculation. The 30 years old invests for 5 years and then decides to cash out. In that case he will invest only Rs 6,0000 and he will take with him Rs 8,1103. What if he choose not to liquidate his investment but does not invest more after the end of five years? He just let’s his money compound till he retires. He would still leave with a retirement corpus of Rs 13.78 lakh. Not a bad deal.

The numbers clearly underline the fact that one should be more focused on investing as much as possible for as long as possible. The magic of compounding then works in the favour of investor. These two factors are in the control of the investor himself. However, while planning their investments most investors would instead chase the rate of return, which is not in their control.

The basic tenets of personal finance emphasis in stocks to generate superior returns. But as stocks are volatile, one needs to have a long term view. If you are keen to generate a high return, long term investing in equity funds are the way out. According to Value Research, a mutual fund tracking entity, multicap fund as a category has delivered 15.43 percent returns over past 10 years. However, if you have a relatively small time frame in the mind, say a year or two then it is prudent to invest in fixed income options. It in turn, reduces expected return on investment. Trying to invest in equity in short term increases the portfolio risk, experts say.

[“source=moneycontrol”]